Southern Construction Framework’s latest market report for the first quarter of the year warns that pricing and supply conditions are now shifting week by week rather than month by month.

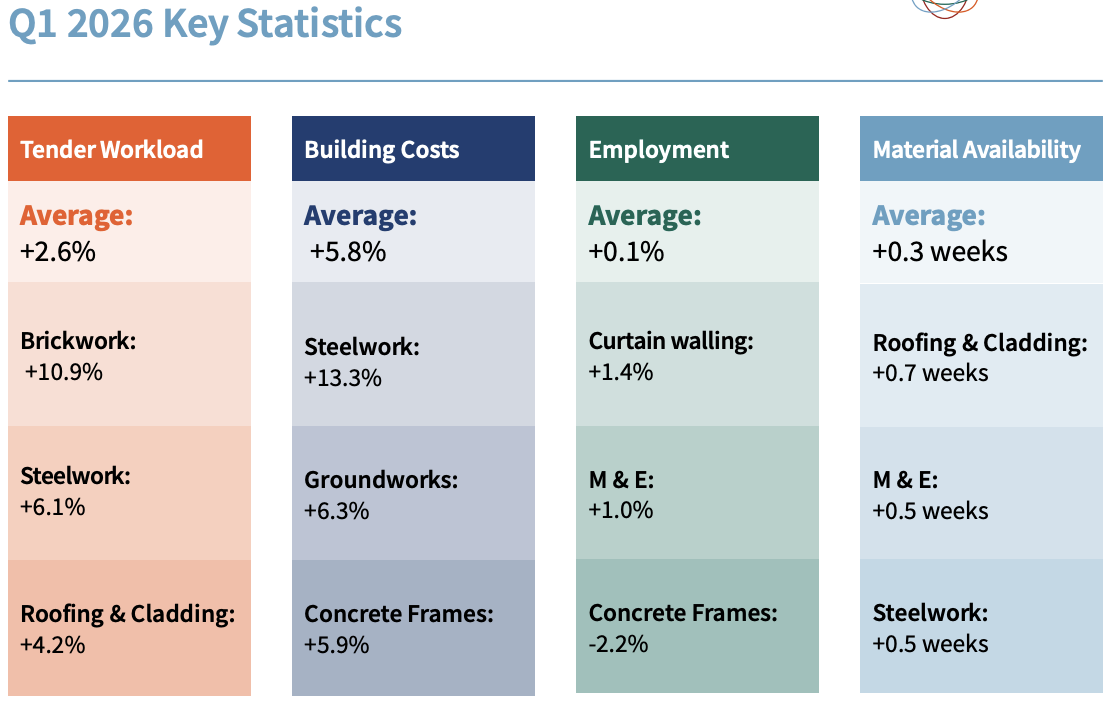

The report, based on a survey of over 150 subcontractors, said tender workload rose by 2.6% during the first quarter as clients continued to test the market and bring schemes forward.

But conversion from tender to site remains patchy as cost pressure, funding gaps and supply chain caution hold projects back.

Build costs jumped 5.8% in the first quarter, outstripping headline UK CPI inflation of around 3%.

Trades with the largest increase included: Steelwork (+13.3%), Groundworks (+6.3%), Concrete Frames: (+5.9%).

Supply chain partners reported they are anticipating steel prices to increase by £300 by Q3 2026, partly driven by anticipated steel import tariffs from July.

Steelwork saw the sharpest increase, rising 13.3%, followed by groundworks at 6.3% and concrete frames at 5.9%.

The report said the Q1 market had entered “a period of renewed volatility” driven by geopolitical instability, disruption to global energy markets, trade routes and investor confidence.

It warned that material availability now needs much closer monitoring alongside prices, as energy costs, supply chain disruption and trade measures continue to feed through to key products.

Residential schemes are under particular pressure, with viability concerns still blocking projects from moving from tender to site.

Janara Singh, assistant framework manager at SCF, said: “Subcontractors told us there is often misalignment between design ambition and budget reality.

“This disconnect is driving repeated value engineering exercises, redesign cycles and extended pre-construction periods.

“As a result, the volume of enquiries continues to grow, while the proportion of projects converting to site remains constrained, contributing to inefficiency and increased bid costs across the industry.”

Firms warned the near-term outlook remains active and fragile, with continued uncertainty around pricing, capacity and delivery.

Build costs are now expected to rise by a further 8% by Q1 2027.

The sharpest forecast rises are steelwork at 11.2%, roofing and cladding at 10% and brickwork at 9%.

Employment levels are also forecast to rise by 5% by Q1 2027 as workloads increase.

But SCF said contractors are deliberately avoiding recruitment until start dates are secure, reinforcing mobilisation delays when schemes do finally move ahead.

.png)

.gif)